What is population covariance?

Beside this, what does population covariance mean?

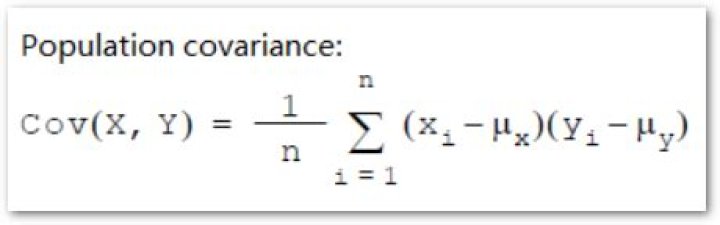

[‚päp·yə′lÄ·shÉ™n kÅ′ver·Ä“·É™ns] (statistics) The number (1/ N)[(v1-vÌ„)· (w1- wÌ„) + ⋯ + (vN - vÌ„)(wN - wÌ„)], where vi and wi , i = 1, 2, …, N, are the values obtained from two populations, and vÌ„ and wÌ„ are the respective means.

Likewise, what is sample covariance used for? The sample covariance is useful in judging the reliability of the sample means as estimators and is also useful as an estimate of the population covariance matrix.

Beside this, what is the difference between sample covariance and population covariance?

1 Answer. Sample covariance matrix is an estimation for the population covariance matrix. As all estimators, it uses sample data and is experimental. On the other hand, the population statistics is theoretical and can be calculated when you know the joint distribution.

What is covariance with example?

Covariance is a measure of how much two random variables vary together. It's similar to variance, but where variance tells you how a single variable varies, co variance tells you how two variables vary together.

Related Question Answers

What is variance and co variance?

Variance and covariance are mathematical terms frequently used in statistics and probability theory. Variance refers to the spread of a data set around its mean value, while a covariance refers to the measure of the directional relationship between two random variables.What is variance in statistics?

Unlike range and interquartile range, variance is a measure of dispersion that takes into account the spread of all data points in a data set. The variance is mean squared difference between each data point and the centre of the distribution measured by the mean.What is covariance and why is it important in portfolio theory?

Covariance is used in portfolio theory to determine what assets to include in the portfolio. Covariance is a statistical measure of the directional relationship between two asset prices. Modern portfolio theory uses this statistical measurement to reduce the overall risk for a portfolio.What is covariance in machine learning?

Covariance is a measured use to determine how much variable change in randomly. The covariance is a product of the units of the two variables. The value of covariance lies between -∞ and +∞. The covariance of two variables (x and y) can be represented by cov(x,y).What is the interpretation of covariance?

Covariance indicates the relationship of two variables whenever one variable changes. If an increase in one variable results in an increase in the other variable, both variables are said to have a positive covariance. Decreases in one variable also cause a decrease in the other.What is the variance of the empirical mean?

The variance of any distribution is the expected squared deviation. from the mean of that same distribution. The variance of the. empirical distribution is. varn(X) = En.What is the difference between population variance and sample variance?

Summary: Population variance refers to the value of variance that is calculated from population data, and sample variance is the variance calculated from sample data. As a result both variance and standard deviation derived from sample data are more than those found out from population data.How do you calculate population covariance in Excel?

We wish to find out covariance in Excel, that is, to determine if there is any relation between the two. The relationship between the values in columns C and D can be calculated using the formula =COVARIANCE. P(C5:C16,D5:D16).Is covariance a correlation?

Covariance indicates the direction of the linear relationship between variables while correlation measures both the strength and direction of the linear relationship between two variables. Correlation is a function of the covariance.What is the difference between sample and population?

A population is the entire group that you want to draw conclusions about. A sample is the specific group that you will collect data from. The size of the sample is always less than the total size of the population.What does a variance covariance matrix tell you?

VERBAL DEFINITIONThe variance-covariance matrix expresses patterns of variability as well as covariation across the columns of the data matrix. In most contexts the (vertical) columns of the data matrix consist of variables under consideration in a study and the (horizontal) rows represent individual records.

What is a population mean in statistics?

A population is a distinct group of individuals, whether that group comprises a nation or a group of people with a common characteristic. In statistics, a population is the pool of individuals from which a statistical sample is drawn for a study. Only an analysis of an entire population would have no standard error.What is the variance of the sample mean?

The variance of the sampling distribution of the mean is computed as follows: That is, the variance of the sampling distribution of the mean is the population variance divided by N, the sample size (the number of scores used to compute a mean). The variance of the sum would be σ2 + σ2 + σ2.What is covariance in probability?

In probability, covariance is the measure of the joint probability for two random variables. It describes how the two variables change together. It is denoted as the function cov(X, Y), where X and Y are the two random variables being considered.How do you convert sample variance to population variance?

When I calculate population variance, I then divide the sum of squared deviations from the mean by the number of items in the population (in example 1 I was dividing by 12). When I calculate sample variance, I divide it by the number of items in the sample less one. In our example 2, I divide by 99 (100 less 1).Is covariance an additive?

The covariance of two independent random variables is zero. Rule 3. The covariance is a combinative as is obvious from the definition. The additive law of covariance holds that the covariance of a random variable with a sum of random variables is just the sum of the covariances with each of the random variables.How do you use covariance?

- Covariance measures the total variation of two random variables from their expected values.

- Obtain the data.

- Calculate the mean (average) prices for each asset.

- For each security, find the difference between each value and mean price.

- Multiply the results obtained in the previous step.